If you're new to blockchain technology, you may be wondering what it is, how it works and if it has the potential to make an impact on your life or work.

As Web3 technology rapidly evolves, we think it's important to debunk the confusion surrounding blockchain technology and explain What is Blockchain in simple terms.

What is Blockchain? Summary:

A blockchain is a ledger, a distributed database that stores information digitally. It is shared with the nodes (operators) of a specific computer network, for example, the Ethereum blockchain.

Blockchains help maintain a decentralised, secure and trusted record of every transaction without the need for centralised third parties.

The Key Features of Blockchain Technology Are:

- A public distributed digital ledger

- Can support decentralization

- Hash Encryption

- Can support full Transparency

- Immutable

- Secure

- Varying degrees of anonymity

- Programmable

- Timestamped transactions

- Consensus Models, i.e. proof of work (PoW)

Blockchain Technology Pros and Cons:

Blockchain technology has many benefits; many view it as a path to a decentralised future. However, it is not without some limitations. Below we list the pros and cons of blockchain technology.

Pros of Blockchain Technology:

- Accuracy: as human interaction isn't involved in the verification process, there is less room for error

- Decentralised Trust: The immutable nature of blockchain technology makes it more tamper-proof

- It offers efficient, secure and private transactions

- Reduced costs as no third-party involvement

- Transparency record system

- No single failure point

- Reduces fraud potential

Cons of Blockchain Technology:

- Running costs: Like any business, there are costs associated with building on the blockchain

- Some networks suffer from low transaction speeds

- Scalability: The triage of speed, scalability, and cost has proved challenging, but solutions are becoming available now

- Security: The distributed ledger is publicly available

- Regulation: There's uncertainty surrounding future legislation regarding blockchain technology

Image source: Shutterstock: Blockchain Technology isn't super complicated.

Page Contents 👉

- 1 What is a Blockchain?

- 2 What is the Difference Between a Database and a Blockchain?

- 3 Blockchain Technology and the Web 3.0 Revolution

- 4 How Does Blockchain Technology Work?

- 5 Why is Blockchain Important?

- 6 What are the Types of Blockchain Networks?

- 7 Is Blockchain Secure?

- 8 How Are Blockchains Used?

- 9 The Pros and Cons of Blockchain Technology

- 10 Conclusion

What is a Blockchain?

A blockchain is a ledger or distributed database shared between the nodes that validate transactions on the blockchain's computer network, and the blockchain stores information in digital format. Blockchains are essential to securing and maintaining a decentralised and timestamped record of every digital transaction on blockchain networks.

The attraction for, and interest in, the blockchain is because of the trust and security of recording data on blockchain platforms without a trusted third party's involvement. Bitcoin was the first to bring a blockchain system into public awareness, and since then, blockchain technology has expanded beyond recognition from those early days.

What is the Difference Between a Database and a Blockchain?

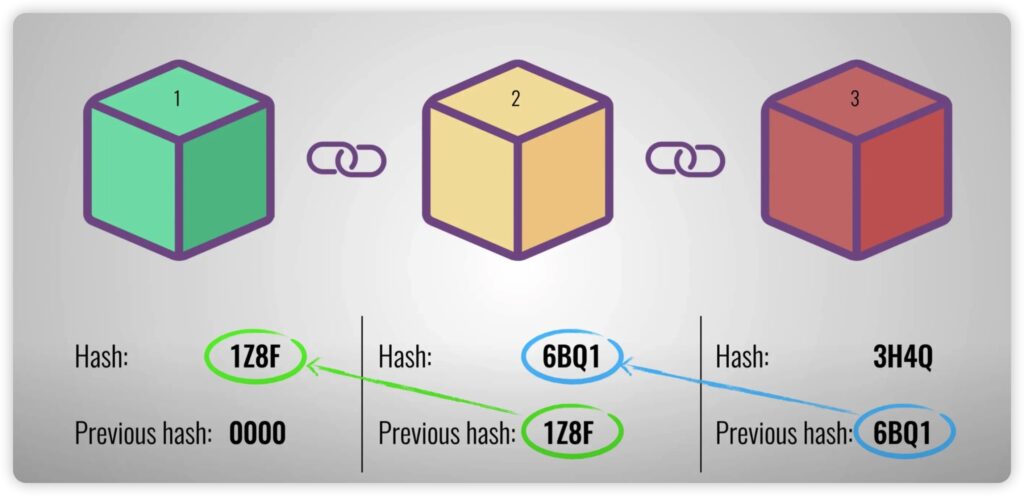

The primary difference is in the data structure. A blockchain gathers data in blocks of information for recording transactions. When a block is complete, it links to the previous block, which forms a chain of data, which we know as the blockchain.

Each new complete block links with the previous block to continue the chain, adding to the timeline of data.

A “normal” database is typically structured by data in tables, not blocks that string together, are immutable and timestamped like the blockchain.

Another key difference is that databases are often highly centralized by an authority, whereas blockchain databases can support decentralization amongst users who can run nodes globally. A Blockchain also uses cryptographic signatures and consensus mechanisms to ensure data integrity and security, unlike databases, which are often able to be altered, adding the potential risk for malicious intent.

Blockchain Technology and the Web 3.0 Revolution

Many people have compared decentralised networks to the third version of the internet. Internet 2.0 was the “internet of information”. People had at their fingertips all of the resources that would usually require a large amount of time to locate. Blockchain technology is now the first step that we are taking towards Web 3.0 or the internet of value.

Web 3.0 is the next evolution of the internet, and many feel it will grow to fundamentally shape and change the future. Web 3.0 is a vast topic to explore, you can find out more about the importance of Web 3.0 and how it integrates with Blockchain technology in our deep-dive article: What is Web 3.0, and Why it Has Insane Potential.

How Does Blockchain Technology Work?

How blockchain works and the benefits of blockchain technologies is to support the recording and distribution of digital information. Blockchain records use DLT (distributed ledger technology), meaning that records are immutable, and nobody can alter, destroy or delete records.

When using the blockchain, users have a wallet with two “keys”, which act as their digital identity for public and private access to their wallet:

A Public Key

This address usually is 34 digits long, a string of digits, and a mix of numbers and letters. You share your public key to receive transactions.

For instance, suppose a friend generously sends you half a dozen of his Bitcoin on one of the public blockchain networks. You give him your public key address, and he organises the transaction. You then receive the Bitcoin and promptly book your private jet to the Bahamas or perhaps a crypto-tax-friendly country.

Sharing your public address is like giving someone your mobile phone number. It's safe, and nobody can directly access your wallet and steal your funds.

A Private Key:

A private key may be a 64-digit hexadecimal code or 256 binary character code.

You do not, under any circumstances, give anyone your private key address. Why? Because if you do, they can directly access your wallet, steal your six Bitcoin, and you can do NOTHING about that except cancel the jet to the Bahamas.

The danger is once a transaction takes place, it is irreversible because of the immutable nature of the blockchain.

Why is Blockchain Important?

Blockchains could revolutionise multiple industry systems. For example, the financial industry is embracing blockchain technology because of the need to respond to the radical changes in the digital world. Blockchain technology can help banks speed up transactions, increase security, offer better financial services and potentially lower fees.

Image source: Shutterstock: There are four different types of blockchain

What are the Types of Blockchain Networks?

There are four main types of blockchain:

- Public

- Private

- Hybrid

- Consortium

Public Blockchain

A public blockchain with distributed ledger technology is permissionless and non-restrictive. It uses a consensus algorithm such as proof of work (PoW) or proof of stake (PoS). Public blockchains are not reliant on an organisation as a network of computers still connects to it. Some public blockchains incentivise users to commit computer power and receive rewards.

A public blockchain is secure and transparent, dependent upon users following the correct methods and security protocols.

The main disadvantage of a public blockchain is the network can be laboriously slow, which can cause higher transaction costs. These blockchains also struggle to scale without significantly impacting the network, which can cause instability. Though advancements in this space are happening all the time, with third-generation blockchains such as Avalanche, Cardano, Algorand, and NEAR protocol looking to overcome the scalability issues that have historically plagued the blockchain industry.

Public blockchains are ideal for non-governmental organisations and businesses built on trust and transparency, such as the financial industry.

Proof of Work Consensus

Bitcoin uses PoW, which involves “miners” working on highly superior computer systems to solve complex problems, verify transactions and create blocks for the blockchain.

The downside of PoW consensus is the phenomenal energy demand. In February 2017, the energy consumption averaged an estimated 10.19 TWh annually. In November 2022, that estimated figure was 115.58 TWh per year (Source: Statista). Though you can find out why many in the crypto community believe this is an unfair criticism and there is much misinformation being spread on the topic by watching Guy's video: Bitcoin Mining: Facts & FUD.

Proof of Stake Consensus

PoS consensus is less energy intensive than PoW. It works because users purchase the cryptocurrency associated with the blockchain and effectively become “stakeholders”, which incentivizes good behaviour and punishes bad actors. Users have voting power on future network decisions and play an active part in securing the network.

A Look at Some of the Key Differences Between PoW and PoS

You can learn more about how these consensus mechanisms work and their strengths and weaknesses in our article on Proof of Work vs Proof of Stake.

Private Blockchain

A private blockchain network is often called an enterprise blockchain or permissioned blockchain. It is controlled by a single entity or works in a closed network or restricted environment, and can implement additional access control layers. Permissioned blockchains can either be fully or partially centralized, the creators can decide on the network's level of decentralization.

Private blockchain networks are somewhat like an intranet whereby a private organisation can determine security, permission levels, accessibility and authorisation. They can decide which nodes have access to change data and block third parties from whatever information they choose.

Private blockchains generally offer faster and more economic transactions than public blockchains due to the fact that they can feature a far fewer number of validators whose nodes can reach consensus faster.

The question is whether a private blockchain network is genuinely a blockchain as an entity controls it, and source codes may be proprietary, which means there is less transparency and less inclination to trust the blockchain. In addition, centralised nodes decide on what information is valid. Private blockchain networks bear more resemblance to traditional business networks.

Use cases for private blockchains are usually companies that want to disallow access to the public, such as auditing, internal voting, such as a DAO and supply chain management.

Hybrid Blockchain

A hybrid blockchain is a combination of a public and private blockchain. Organisations can set up a public permissionless system alongside a private, permission-based system, giving them control over who accesses stored data.

A hybrid blockchain is not transparent. When users join a hybrid blockchain, they are anonymous until they create a transaction, in which case, their identity becomes public.

Transactions are not available to the public but are timestamped and verified if required, for example, by allowing access via a smart contract.

Unlike a public blockchain, hackers cannot control 51% of the network. A hybrid blockchain is easily scalable, fast, and cheap.

Ideal use cases for hybrid blockchains are retailers, medical records, real estate, and governments. These entities can retain system privacy whilst giving the public access to information as required.

Consortium Blockchain

A consortium blockchain is not dissimilar to the hybrid model as it has public and private features. The core difference is that multiple organisation members can collaborate on the network. One entity does not control the blockchain, which eliminates many risks and means that the blockchain is technically decentralised.

Though it doesn't have the transparency associated with a public blockchain, a consortium blockchain is secure and imminently more scalable.

Typical use cases include payments and, banking, supply chains, and the health industry.

The main attraction for organisations switching to blockchain technology is the decentralised nature and security. Still, we cannot assume that the blockchain is 100% safe from hackers, so let's explore blockchain security.

Is Blockchain Secure?

Blockchain technology achieves decentralised security and, by default, trust. Completed blocks are added linearly to the end of the blockchain in chronological order. Once added, it's practically impossible to change the contents of a block.

Each block contains a timestamp, its own hash, and the previous block's hash.

Hold on, what's a hash in simple terms?

A hash is an essential function of the blockchain. It is necessary for the encryption needed for information security. Hashes are always a fixed length and practically impossible to guess.

A hash is a function that meets the encrypted demands needed to secure information. A mathematical function creates the hash code, so digital data becomes a string of letters and numbers. If that information is edited, it changes the entire hash code. Here is a great image from Simply Explained, diagraming a Hash:

Image via Simply Explained- Savjee

When Bitcoin began, the hash code difficulty was 1. It was simple for most miners to solve. Today, the Bitcoin hash code is 43.05 trillion (Source: Coinwarz). Bitcoin miners receive rewards if they get the closest to solving the hash code, but imagine the challenges with today's difficulty levels.

Hackers have developed sophisticated tools and techniques to hack Web3 systems. However, suppose a malicious hacker (a bad actor) runs a node on the network and tries to change the blockchain to steal digital assets or data.

If the hacker manages to edit their copy of the blockchain, it cannot be cross-referenced with the other nodes. Consequently, the hacker's copy stands out like a sore thumb on the network. Immediately, the nodes would invalidate the copy as malicious.

Further, to hack the blockchain, a hacker would have to have control of and change 51% of the blockchain copies for their copy to become the majority. An attack like this would be challenging, prohibitively expensive to organise and require significant resources. For instance, all the blocks would have different hash codes and timestamps, which would be a logistical nightmare.

Hacking a blockchain would be equivalent to trying to rob a bank when a hundred police officers are standing at the teller's desks. As soon as the robber did something suspicious, he'd be spreadeagled on the floor and dragged off to the cells.

Another thing to consider is if the hacker holds tokens associated with the blockchain, they could lose their entire holdings. Nodes working on the network can create a hard fork, deflecting the attack by creating a new chain separate from the one the hacker is trying to change.

Though it's not impossible for a hacker to gain 51% of control of a blockchain, it's less likely than trying to hack a traditional database. Security is one of the major pros of the blockchain and a core reason for so many organisations switching to blockchain technology.

Image source: Shutterstock: The blockchain is secure, transparent and decentralised.

How Are Blockchains Used?

Many companies have adopted blockchain technology to improve systems and processes, for instance, IBM, Microsoft, Pfizer, Unilever, Amazon, Siemens and many more.

There are unlimited use cases for blockchain technology, but the following are a few examples of how blockchains are used.

Banking and Finance

Financial institutions incorporate the blockchain to secure data and provide faster transactions. The blockchain operates 24/7, so transactions can continue when financial institutes' offices are not open. For example, you can deposit a cheque that instantly shows in your account.

Blockchain technology can provide many financial services without third-party involvement in monitoring transactions, and that comes with multiple benefits:

- Automation frees banks to focus on other activities instead of monitoring payment transactions.

- Reduced costs: Blockchain can provide faster and cheaper transactions than traditional banks.

- Faster transactions: It is easier to use blockchain for speedy transactions for fundraising, settlements, borrowing and lending, trade finance, credit etc.

- Better security: As two security keys are required for transactions, it adds a layer of extra protection, and once verified, nobody can alter data.

- Digital currencies: Banks worldwide are exploring implementing CBDC (central bank digital currency) as standard currency.

- Reduced risk of fraud: As all transactions are verified, recorded and immutable, the blockchain can help prevent the misuse of funds by altering information.

- Reduced errors: Transactions are easily reconcilable on the blockchain, so banks can find them before completing a transaction. This benefit saves time, especially when auditing.

Cryptocurrency

There are over 22,000 cryptocurrencies listed on Coinmarketcap, and the blockchain has been the foundation for many crypto startups. Blockchain technology enables cryptocurrencies to exist and operate without a central authority.

Cryptocurrency has become a lifeline for countries lacking financial infrastructure and unstable currencies, making financial opportunities available worldwide.

For example, leading cryptocurrency exchanges, like Binance and kuCoin made headline news by supporting Ukraine with millions of dollars of cryptocurrency donations. Cryptocurrency donations were able to reach the Ukranian people far faster than what was possible using traditional banking transfer methods. The Ukrainian people have also turned to cryptocurrencies for day-to-day expenses as their banking infrastructure has been interrupted by the conflict.

Smart Contracts

Smart contracts are computer codes built into a blockchain to help verify, negotiate or facilitate a contract agreement to a specific set of conditions that users must agree upon to enable the smart contract to fulfil its purpose.

For example, suppose a real estate agent requests a deposit on a house from a buyer. The agent then offers to remove the listing from the market. The buyer sends the security deposit to the smart contract, and the real estate agent sends the agreement. If one-half of the parties fail to do as required, the smart contract returns the money or the agreement, depending on which party failed.

The use cases and utilities for smart contracts are endless. Any agreement or contract needed between two or more parties can be coded into and executed automatically using smart contracts, completely removing the need to “trust” the other party involved.

Healthcare

Healthcare providers increasingly use the blockchain to store patients' health records, stored with a private key and not publicly available. There are also known use cases of hospitals and medical universities using NFTs to collaborate globally and study the cause of genetic mutations in human DNA.

Supply Chains

Supply chains can be complex and messy, and difficult to track information, such as materials' authenticity. The blockchain can efficiently follow each stage of the supply chain, with timestamped junctions to keep the supply chain moving. You can learn more about how blockchains are revolutionizing the supply chain industry in our VeChain review.

Voting

Centralised voting systems are often questioned regarding authenticity as it isn't a huge challenge to “fix” results. The blockchain creates an immutable voting record that cannot be tampered with and is a more authentic system for voting.

Image source: Shutterstock: Is Blockchain the future for business?

Data Protection

Having all of your data stored in a centralised location can make you an easy target for hackers. The past two years have shown us the catastrophic impact of data breaches at a number of companies and government organisations.

With blockchain technology, the nodes are all spread out across the network and hence are harder to compromise. A potential application of the technology is the DNS system. Given that these rely on caching, they are vulnerable to DDoS attacks. There is no need for caching when blockchain technology is used, and we are seeing enterprises and individuals increasingly turning to blockchain solutions for data protection.

Digital Identities

Nearly everything we do online makes use of our identity. Websites and services need to authenticate exactly who we are in order to assist us better. Of course, this can be inefficient and dangerous. Hackers usually target consumers with phishing tactics in order to get personally identifiable information.

Distributed ledgers allow us to have a more efficient and secure way of identifying who we are. Blockchain also hands back control of our personal data to us without having it stored in a central location. Moreover, when this digital identity is stored on the blockchain it is immutable which means that no one can alter it for malicious purposes. Vitalik Buterin, the creator of Ethereum, supports the idea of a digital identity in the form of an NFT in what he refers to as Souldbound tokens, which is an intriguing concept.

Data Storage

Space is an increasingly sparse resource which we often run out of. However, across the internet, there are millions of computers that have extra storage space that is not being utilised. This is essentially a wasted resource that one is not making the most use of. Moreover, when you make use of cloud storage solutions such as Dropbox, they can and have been hacked as they are centralised.

A decentralised blockchain solution to online storage is the only way that we can take advantage of this unused space in a secure manner. For example, a recent ICO of Filecoin raised a record of $257m for its decentralised storage concepts. They will no doubt be taking on the established giants in the cloud storage space.

Blockchain technology has many benefits but has some downsides, so let's discover the pros and cons in detail.

The Pros and Cons of Blockchain Technology

Blockchain technology continues to evolve. A blockchain network remains the foundation as multiple Web3 startups emerge with ever-increasing, mind-blowing technology. We know there are many benefits, but duality exists in blockchain, too, so there are pros and cons associated with the blockchain.

The Pros of Blockchain Technology

Accuracy

The nature of the blockchain is to have a vast network of nodes working together, all supplying computer power, verifying transactions and completing blocks. If a mistake occurs or a malicious node interferes with the chain, other nodes can immediately observe the error or attack and create a hard fork to protect the network.

Eliminating human error from the verification process is a formidable bonus for many organisations.

Decentralised Trust

The immutable nature of blockchain technology makes it more tamper-proof than traditional data systems. When transactions register in shared ledgers, it is impossible for anyone to alter them. If an error occurs in a transaction, the only way around it is to create a new transaction that reverses the first one. Naturally, because of the nature of the ledger, both transactions are timestamped and available publicly. In the case of transaction records that include errors, a new transaction must initiate in the reverse order, and the transaction is also displayed.

Efficient, Secure and Private Transactions

Blockchain security and privacy help to create trust in a network. In our centralised society, we're accustomed to third-party monitoring of our actions and are getting to like that less. The blockchain is fast attracting more businesses and members of the public because of these core features.

Reduced Costs as no Third-party Involvement

Generally, the blockchain is more cost-effective because no middlemen are involved. The nodes keep the system running smoothly and are often rewarded for their engagement, creating a streamlined system.

Transparent Record System

The blockchain creates a genuinely transparent environment as every transaction is timestamped, recorded, and immutable.

No Single Failure Point

Every node on a blockchain network works in line with the other nodes. If one node fails, it is immediately apparent. A blockchain cannot fail if one node makes a mistake, which creates a highly secure network with no single failure point.

Reduces Fraud Potential

As mentioned earlier, a hacker would need to gain control of 51% of the network to alter information. With a vast distributed network of nodes, it is almost impossible to achieve.

Image via Shutterstock

The Cons of Blockchain Technology

Costs

Because of the significant computing power, blockchain running costs can be prohibitive. However, there are administrative costs associated with any business, and companies planning to build on a blockchain, such as Ethereum, don't automatically adopt the running costs of the blockchain. You could compare it to a company renting commercial space. They pay rent but aren't responsible for the running costs of maintaining the building.

Varying Transaction Speeds

The Bitcoin blockchain is notoriously slow as PoW is labour-intensive. According to Statista, transactions can take 40 mins per transaction and can vary greatly depending on network use.

Compare Bitcoin transaction speed with Polkadot, which operates a proof of stake consensus {PoS) and has transaction speeds of 2 minutes. Some cryptocurrencies were created with speed in mind, with some blockchains like Avalanche coming in at a 2-second transaction time, or networks like Solana and XRP, which have nearly instantaneous transaction settlement times, making them far superior to any transfer method available in the traditional financial system.

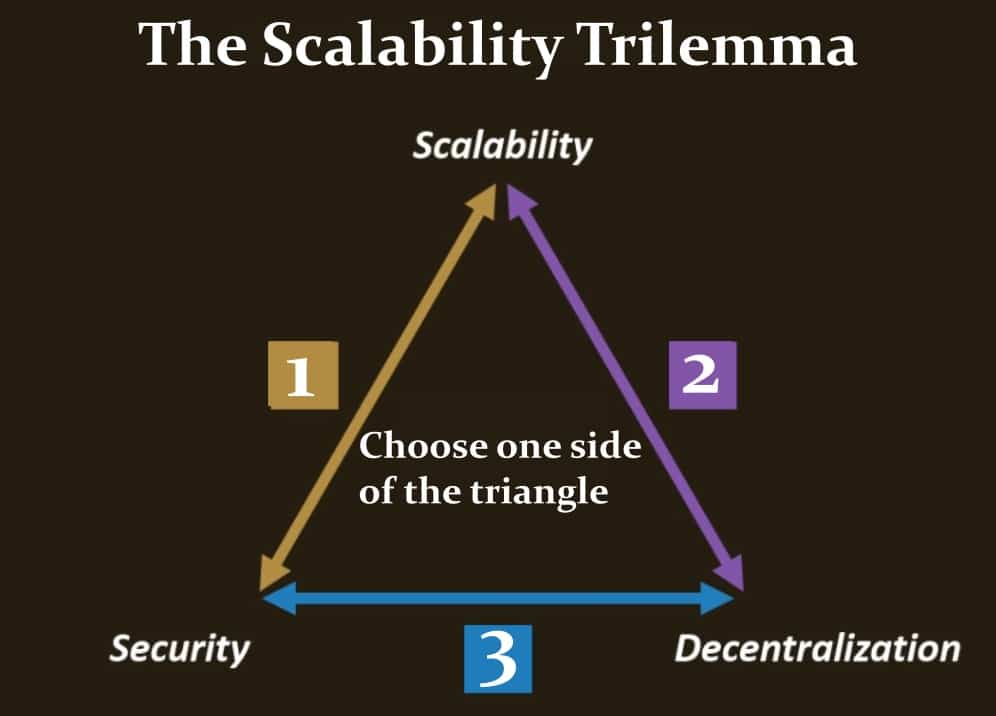

Scalability

The triage of speed, scalability, and decentralisation has proved challenging. Many blockchains have tried and failed to scale, primarily because one “leg” collapses. Ethereum transitioned from PoW to PoS over several years and experienced many setbacks before completing the transition.

The Blockchain/Scalability Trilemma has Proven to be a Problem for Blockchain.

The image above shows what is known as the blockchain or scalability trilemma. This has proven to be the “Everest” of problems, a hurdle faced by all blockchain networks. You can learn more about the trilemma and how projects like Algorand are taking an interesting approach to overcome this hurdle in our Algorand Review.

For any business to succeed, it needs to scale, and it continues to be problematic for many blockchains.

Security

The distributed ledger is publicly available. Although transparency is a positive of the blockchain, having everything publicly available is not ideal for every organisation.

Regulation

There's uncertainty surrounding future legislation regarding blockchain technology. Governments worldwide are concerned about the decentralised nature of the blockchain, primarily because they have no control over it.

There is a constant push from the SEC and other worldwide governmental organisations to discover a loophole they can challenge to stop blockchains from continuing with claims of decentralisation.

Image source: Shutterstock: There are over 1,000 different operational blockchains.

Conclusion

Blockchain technology is hopefully here to stay. Bitcoin and Ethereum are the top two blockchains listed and two of the most well-known and respected blockchains worldwide.

Today, new blockchains have embraced the learning from blockchain pioneers, trying to find ways to make a blockchain more scalable, affordable, and effective. Though Bitcoin has its challenges that Bitcoin developers are working to overcome surrounding costs and environmental issues, it remains the leading blockchain in the space and will likely stay in the top spot.

Organisations across the globe, eager to stay ahead of the game, are exploring blockchain technology, embracing NFTs, the metaverse and all things associated with Web3.

It will be interesting to see what happens over the next few years as artificial intelligence and machine learning catch the public eye and detract from the blockchain momentarily.

We hope you now understand more about blockchain technology, and we have given simplicity to the subject.

What is Blockchain? FAQs

What is a Simple Explanation of the Blockchain?

Think of the blockchain as a publicly available decentralised database or ledger that stores data electronically, securely recording every transaction digitally without intermediaries. Each blockchain has a distributed ledger of its own.

What is the Main Purpose of Blockchain?

The primary purpose of a blockchain protocol is to organise and securely store trusted records without third-party involvement, while also processing transactions of data in a trustless and tamper-proof manner.

What is a Blockchain in Simple Words?

A blockchain is a decentralised database that records every transaction digitally and timestamped.

How does Blockchain Work in Simple Words?

The simplest way to describe the blockchain is that it acts as a decentralised public ledger by recording every transaction via multiple computers.

What is an Example of Blockchain?

Blockchain technology is often used in banking and financing. For example, Santander launched “Santander One Pay FX”, a blockchain-based money transfer service in 2018, which enables customers to make next-day international or same-day money transfers. Blockchain is the underlying technology behind cryptocurrency networks like Bitcoin, Ethereum, and thousands of others.

How Does Blockchain Generate Money?

It varies. Some blockchains make money by using SaaS (software as a service). Other blockchains work with clients on custom projects, earn from transaction fees or develop software solutions for enterprise clients.

What is the Primary Difference Between Cryptocurrency and a Blockchain?

Cryptocurrency is a virtual or digital currency that uses cryptography for securing transactions. The blockchain is a decentralised ledger that securely records across a distributed computer network of nodes (operators). For example, Ethereum is the blockchain, and the network's cryptocurrency is $ETH. Cryptocurrency can be thought of as the currency that runs the blockchain network, which incentivises and acts as a medium of exchange for operators on the blockchain.

Is Every Crypto a Blockchain?

No. Every blockchain has a cryptocurrency associated with the ledger. For example, Bitcoin is the blockchain, and $BTC is the cryptocurrency associated with the Bitcoin blockchain. Other tokens can run on top of a blockchain, many of which do not have their own blockchains. For example, there are tens of thousands of cryptocurrency tokens that run on top of the Ethereum network. These cryptocurrencies do not all have their own blockchain but use the Ethereum blockchain.

Here is a great article from Ledger that explains the concept of Coins vs Tokens in greater detail to give you a better understanding.

Why is Crypto Called Blockchain?

They are separate things, but many people do not understand the difference. Crypto is a digital or virtual currency, and blockchain is like the operating system, a distributed ledger that operates through a network of computers.

Who Invented Blockchain?

Satoshi Nakamoto is the anonymous creator of Bitcoin, the first instance of blockchain technology in 2009 when you could purchase Bitcoin for less than a dollar. The consensus is that Satoshi Nakamoto is likely a group of people working together to create Bitcoin. The true identity of a person or persons is still unknown.

How Many Blockchains are There?

There are at least 1,000 different blockchains. The largest and most well-known blockchains are: –

On some blockchains, it's possible to create multiple tokens. For example, over 20,000 different tokens are built on Ethereum's blockchain, with the highest number of developers on the network.

What's the Difference Between Blockchain and Bitcoin?

Bitcoin is a blockchain, as is Ethereum, for instance. The blockchain is the underlying technology that enables, for example, cryptocurrencies, smart contracts, and NFTs.

What is a Block on the Blockchain?

Transactions occur in “blocks” of data and are moveable assets. These can be tangibles, such as a product, or intangible, such as an NFT.

A block is simply a data structure with the blockchain database permanently recording each transaction. Each block links to the next, creating a chain of blocks that are securely timestamped and recorded on the blockchain.